A simple financial setup guide for clueless high income earners

Do you have a bunch of cash sitting in a high-yield savings account? And you have no idea what to do with it? Well this blog post is for you!

This blog post was inspired by a couple of friends and coworkers figuring out how to manage their money.

It’s not for day traders or people trying to gamble. It’s not for people struggling to live below their means. There are plenty of resources for you, but this is not the correct place to look. You’ll need a fair chunk of cash to implement the contents of this blog post. If this ain’t you, stop reading!

Here’s the situation I see way too frequently:

You’re a (relatively) high earner who lives well below your means.

You’re probably sitting on a pile of cash in a high-yield savings account, and you probably have a concentrated position on a single company’s stock (i.e. your employer).

While you’re not in financial trouble, the lack of a strategy makes you nervous about the future. You want a simple, idiot-proof, low-maintenance strategy that just works.

Fortunately, it’s not that hard.

The strategy

Calculate and save up an emergency fund (3-6 months of expenses). Keep that in a high-yield savings account.

Pay off any remaining debts.

Figure out if you’ll need a lump sum of cash in the future (e.g. to buy a house).

Max out your tax-advantaged retirement accounts (e.g. 401k, HSA, mega-backdoor Roth).

Chuck any surplus cash into a taxable investment account.

Go touch grass.

Hopefully the first three steps should be simple enough. Usually it’s the investment part that trips people up. (“Where do I put my money? What do I buy?”)

What do I do? Where do I put my money?

Prioritize contributing to retirement accounts because of the tax benefits. Understand how much money you need for spending and how much you have to spare for investing. Then it’s time to click some buttons.

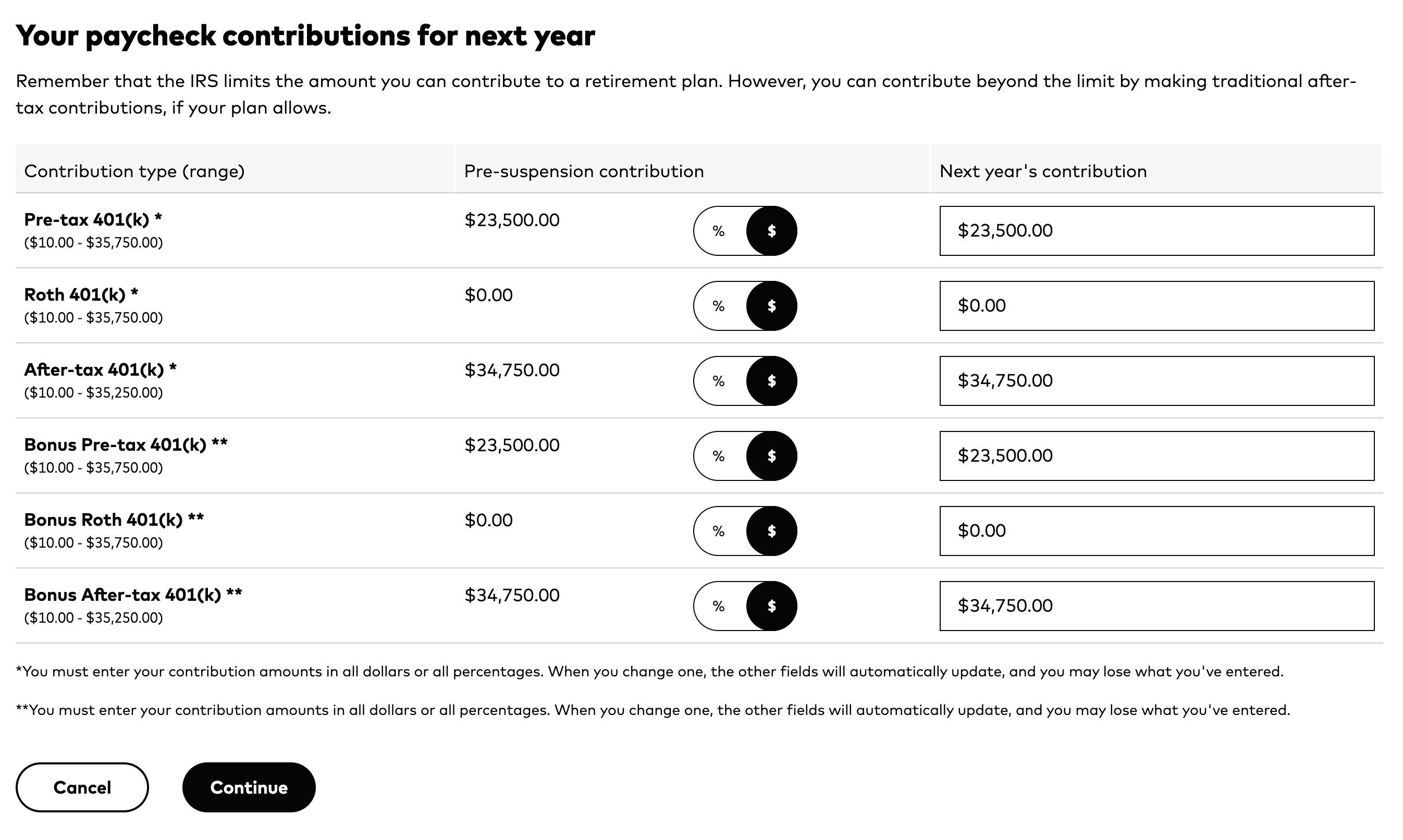

401(k)

The first place you’ll want to put invest is into a 401(k). Max it out. You’ll probably get employer matching. It’s free money.

You should aim to max out your 401(k) every year. That’s around $24k of contributions per year at the time of writing. Any contributions to the 401(k) must come out of your paycheck, and you typically configure the contribution amount/percentage via your brokerage.

How you spread out your contributions is up to you. What matters is that you max out the account by end of year. Personally I try to max things out as quickly as possible: at the start of the year, I hold on to some cash and then contribute 100% of my paycheck until the retirement accounts are maxed out.

“Should I contribute to a pre-tax 401(k) or Roth?” I’ll be honest, it really doesn’t matter. Flip a coin. Or if you’re too lazy to flip a coin, just pick Roth. The difference in the long run is minuscule and situationally dependent. The math needed to figure out what’s optimal for you isn’t worth the time, in my opinion.

Mega Backdoor Roth IRA

Maxed out your 401(k)? Great job! If your employers supports the mega backdoor Roth IRA and you still have money from your paycheck that you don’t plan to use, you can continue to contribute parts of your paycheck up to the IRS limits.

I’ve written about the mega backdoor Roth IRA previously, so I won’t harp on it too much here. Just make sure it’s actually offered by your employer, and make sure you have the money to spare. As of the time of writing, it’s an additional $35k of contributions after maxing out your 401(k).

The Mega Backdoor Roth

If you're lucky enough to work at a company with a generous 401(k) policy, you might be able to take advantage of a wonderful investment mechanism called the mega backdoor Roth IRA. Each year, you can contribute a large chunk of money that grows tax free until the end of time. Nice!

Unlike the 401(k), contributing to a mega backdoor Roth isn’t for everyone. There’s no employer matching, and the limit you can contribute is quite high. Do not max out a mega backdoor Roth IRA if you expect you’ll need that $35k within a few years.

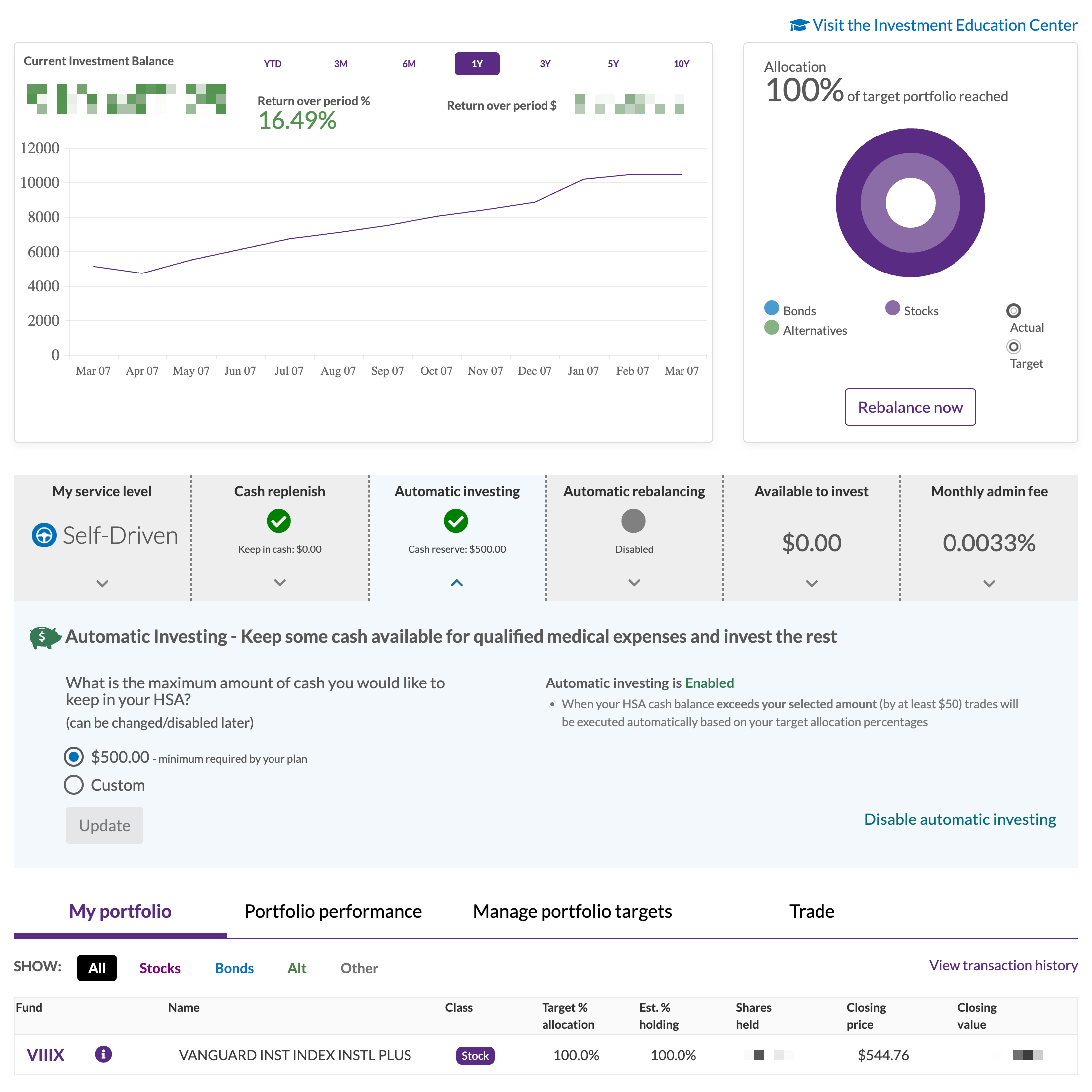

HSA

It’s a bit less obvious, but a Health Savings Account (HSA) is a tax-advantaged investment account. I recommend young and healthy people opt for an HSA if possible. You can contribute money from your paycheck into your HSA. Your employer probably contributes money into your HSA as well.

With your HSA money, you can spend it on medical expenses, but you can also invest the money. If possible, max out your annual HSA contributions, and set it to auto-invest. Even if you don’t expect to get sick, it’s a great avenue for future medical expenses. And transferring an HSA to your children doesn’t get taxed, so you can really stick it to Uncle Sam.

A side note on HSAs: if you have medical expenses, prefer to pay with “normal” money rather than withdrawing from your HSA. You should be careful about taking money out of a tax-advantaged investment account. You won’t get an opportunity to put it back in.

Taxable accounts

You’ve maxed out your 401(k), the mega backdoor Roth, and your HSA. And you still want to invest more? You absolute stud! Maybe you can just Venmo me the extra money instead.

On a more serious note, you don’t want to hold surplus funds as cash for too long. Open up a brokerage account. Any will do. I recommend a large brokerage with a shit UI. The shittier the UI, the less tempted you are to fuck around. Brokerages with nice UIs encourage you to constantly look at your money, which is a recipe for doing something stupid and ruining years of compounding.

Vanguard, Fidelity, and Schwab all work great. If you already have an employer account with a broker, it’s easy to open up a personal account with them too. (For example, Google employees might prefer a Schwab account, since that’s where their stock goes.) Interactive Brokers also works, but its UI is too shit, even for me. Avoid Robinhood; its UI is too nice. M1 Finance is fine (because of their auto-rebalancing features), but be careful since their UI is nice. Most importantly, use my referral codes so I can afford guac on my Chipotle burritos.

Investing: what do I actually buy?

Investing is important. If used correctly, money compounds. When it comes time to retire, you want to live off your compounding nest egg. Compounding takes time, so try to invest as much as you can as early as you can.

The two greatest mistakes in investing is (a) taking too much risk and (b) not taking enough risk. Understand your personal risk tolerance. The Bogleheads and Reddit /r/personalfinance wikis are great starting points for further reading.

Here’s what you do:

Pick a low-cost, diversified index fund (or funds).

Put your investment cash into said fund(s).

Periodically deposit more funds into the portfolio and rebalance as necessary.

What’s in Andrew’s portfolio?

In Skin in the Game, Nassim Taleb made a great quote about investing advice. “Don’t tell me what you think, tell me what you have in your portfolio.” Here’s what I have in my portfolio:

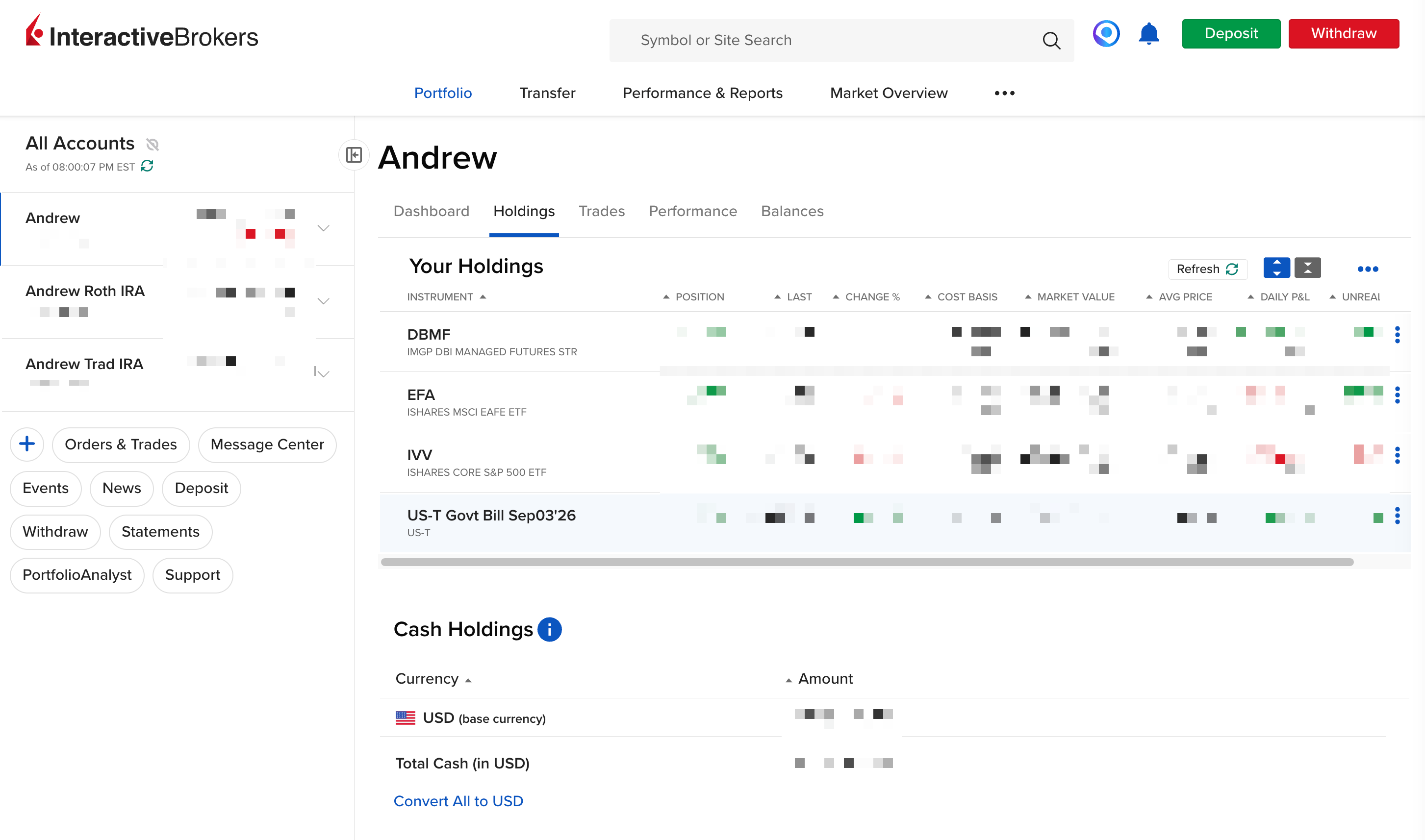

I hold IVV/EFA/DMBF with a 50/50/50 allocation. Three positions. That’s it. All equally weighted. My taxable portfolio is 1.5x leveraged (hence it’s not a 33/33/33 allocation). For every two dollars I have, I borrow one dollar on margin. Do not take leverage if you don’t know what you’re doing. Taking leverage can fuck you and kill decades of progress. You can get by just fine without leverage.

For my tax-advantaged portfolios, it’s a lot simpler. I just go 100% in the S&P 500. No leverage. It’s all auto-invested. My two investment accounts are my 401(k) and my HSA. In my 401(k), the portfolio is completely in Vanguard’s S&P 500 proxy. In my HSA, the portfolio is completely VIIIX, which is some other S&P 500 proxy. The exact fund doesn’t matter: VOO, IVV, or some other S&P 500 proxy will all have 99.9% correlation. These were not deliberate strategic decisions on my part; I just picked whatever S&P 500 proxy was available.

Why do I do what I do?

I have a stake in both domestic index funds and international index funds. Having exposure to both domestic and international equities obviates the need for bonds.

I have a stake in a managed futures strategy as a hedge in situations where equities perform poorly.

I leverage 1.5x such that I magnify returns without suffering from volatility drag.

For my retirement accounts, my position is much simpler because retirement accounts can’t take leverage. (Also I have a financial advisor managing my taxable account, and I’m too lazy to do anything fancier for my retirement accounts.)

Don’t blindly copy me. I’ll give you suggestions in the next section. If none of this made sense to you, don’t stress out.

Recommended example portfolios

In my examples, I’ll use VOO to represent the S&P 500 (i.e. domestic) index and VXUS to represent the international index. There are many funds that track the same index, so when you buy for yourself, you don’t need those exact ticker symbols.

I present to you the 1-fund portfolio and the 2-fund portfolio:

The 1-fund portfolio: 100% in VOO

So simple! You literally can’t go wrong with this. The S&P 500 is already super diverse.

In your retirement accounts, you can opt to go for a target retirement date fund as well. It doesn’t really matter.

The 2-fund portfolio: 50/50 in VOO and VXUS; equally weighted

This is good if you want international exposure.

This is also good if you want to scratch that itch with having more than 1 position in your portfolio.

Why have a 50/50 allocation instead of 60/40 or something else? Because 50/50 is simple. People will debate all day about whether to hold more domestic or international equities. Don’t waste your time, and instead go for a “good enough” portfolio.

Did you expect something more complicated? I sure hope not. These are set-it-and-forget-it portfolios that will make you a very happy camper over a long time horizon.

It’s hard to go wrong since you’re sufficiently diversified. Diversification is the only free lunch in investing. Do not take leverage. If you find this blog post informative, you’re not ready to handle leverage. Your goal is the match the index, not beat it. The best strategy to match the index is to buy the index.

Maintenance

Investments into retirement accounts should be fully automated. Contributions will come straight out of your paycheck. You may need to adjust contributions once a year, since IRS limits change and health insurance policies change.

For personal investment accounts, try not to mess with it too frequently. (Every month or quarter is perfectly fine.) Ideally you rebalance around the same time you get a cash infusion (e.g. every other paycheck). When rebalancing, buy positions in your portfolio that are underweight; try to avoid selling overweight positions. Most brokerages have some form of auto-investing that will track a target portfolio allocation. So ideally, you’ll have to do very little manual decision-making in general.

If a part of your compensation is in company stock, sell the stock as soon as it vests and reinvest the proceeds. Some companies offer auto-sell programs so you only need to handle reinvesting the cash. I know of many people who are hesitant to sell company stock. It’s a rabbit-hole of a debate, and I won’t go to deep into it. If you had the cash, would you buy back the stock? If not, then you should diversify. Furthermore, you organically incur concentration risk with your employer, even without the additional concentration risk from holding too much of a single stock.

At this point, everything should be automated and diversified. Great! Pat yourself on the back. Now we proceed to the most important step: STOP THINKING ABOUT INVESTING and go touch grass. Money is a means to an end. You’ve set yourself up for success. Now go live a good life.